Paymentology

1-05-24

Any business that decides to run its own card programme would need to invest in the right financial licensing, scheme membership and have internal expertise on running payment programmes. While all of this is possible, it would be impractical for most organisations and would come at a high cost.

The more economical and efficient option would be to look to a trusted third party. Paymentology's guide to card programme management provides a more in-depth explanation of the role and duties that card programme managers perform, but in summary these entities act as a hub for businesses launching their own card programmes, managing all of the relationships necessary to plan and carry out the project successfully.

In this blog, we'll look at various industry sectors and their respective use cases for card programmes. And if you want to know more about how Paymentology can help you get your card programme set up then get in touch.

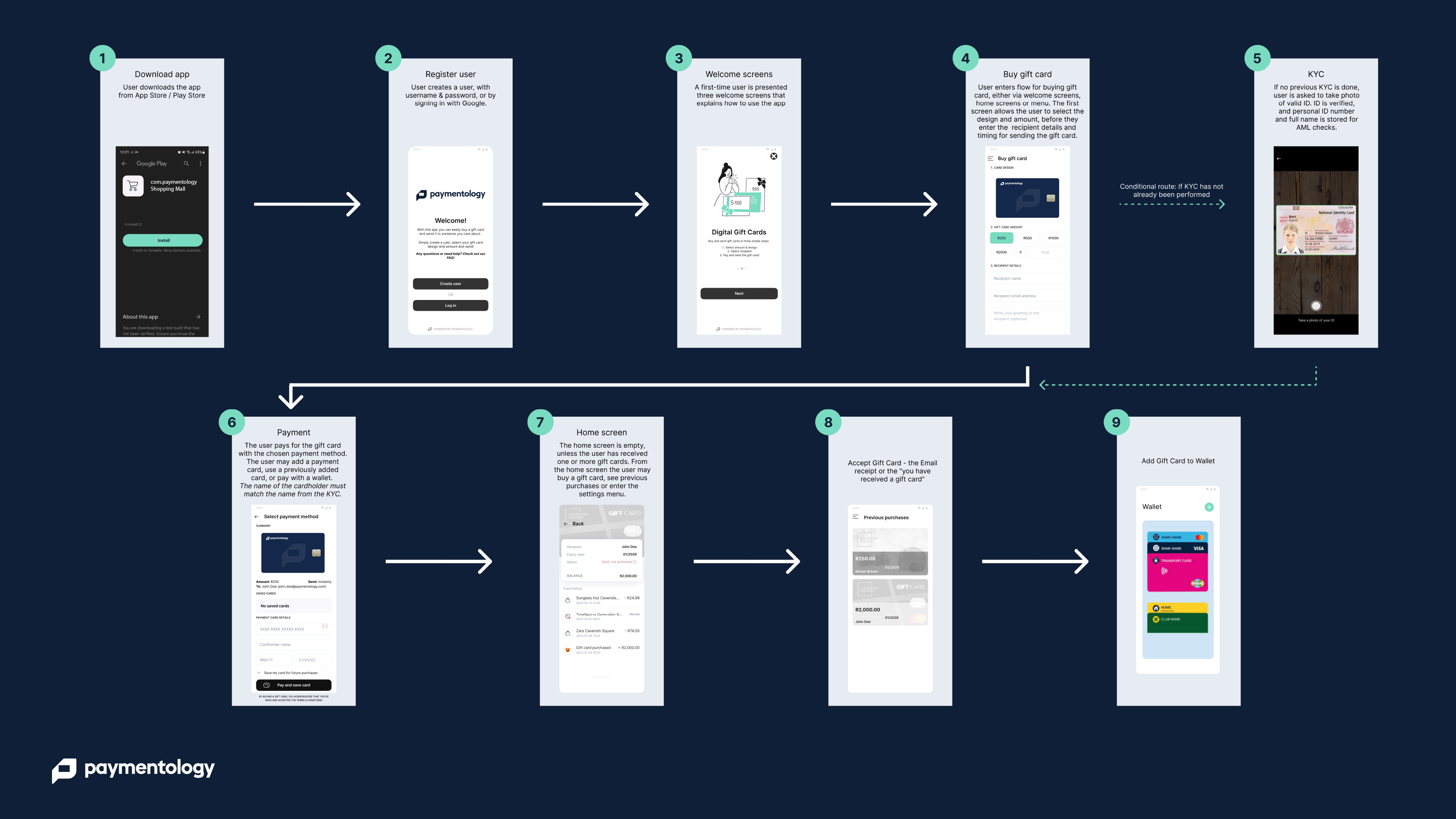

Shopping malls and retail brands need to drive customer loyalty. While some large supermarket chains offer credit cards and banking services, smaller retailers can now set up card programmes, allowing them to issue prepaid cards, gift cards and store value cards in virtual and physical form.

A card programme is an ideal route for insurers that want to digitise their policyholders’ experience. Virtual cards can be issued as a payout mechanism, offering a lower cost route to delivering payouts to the people that need them, for the products and services they need, at the time they need them.

Fintechs active in areas such as payments, financial inclusion, and Buy Now Pay Later (BNPL) look to card programme managers to issue cards and handle the entire payment process, while they can focus on building their own digital experience. This allows them to launch more quickly, keep costs low and offer superior payment experiences that they would not have been able to build on their own.

To succeed in the new digital world, card programme managers bring a holistic solution to help money transfer operators (MTOs) offer a competitive service for customers while keeping costs low. Prepaid cards are a cost-effective way to include underserved segments in low income areas. Branded in collaboration with an international card network such as Visa or Mastercard, payment cards can also help customers access international payments when travelling as well as access to cash from ATM networks.

Often seen in the nonprofit sector, many microlenders focus on lending to women, minorities, and other underserved entrepreneurs. Microloans work like regular business loans, except they’re not issued by traditional banking institutions. Card programme managers are useful to microlenders as they help solve many of their challenges, bringing the regulatory framework to enable loans to be made digitally. Card programmes can handle the entire payment process for issuing these payments either virtually on a mobile phone or in person. This model helps reduce costs and ensures the efficient distribution of recurring loans on digital or physical cards that can be topped up.

Corporations need better solutions for managing corporate expenses, travel, payroll, and supplier payments. Card programmes provide corporations with enhanced control over spending, with each card assigned to a specific employee or supplier and payments allocated to designated budgets. Spending limits can be set, and all expenses are processed and approved or rejected centrally, streamlining the financial management process for these businesses.

For governments that wish to distribute grants and bursaries digitally, card programmes offer a smart way to serve students through student payment cards. Students benefit from a payment method to receive the funds, while funds can also be limited to certain purchases; for example payment for an assigned college, purchase of equipment at partner libraries or stores, accommodation payments and the like.

These are just some examples of how different organisations can use card programmes to serve their customers, boost loyalty, create new revenue streams and enable financial inclusion. If you'd like to know more about how card programme management works, then download Paymentology's guide to card programme management or get in touch today.